Mobility

has to be embraced by the Financial Services Providers (FSPs) is clear to all.

The big questions are how, when and for what services. This article gives some

broad analysis to address these questions. The findings are that financial

Information based services should be embraced immediately; the transactional

services should be the medium term goal, i.e., within 6 months to a year, and

finally by 2003 FSPs need to embrace the full customer relationship including

one-click transaction, live advice, personal mobile Ads, and third party

sales.

The Financial Services Providers (FSP) including banks,

Investment institutions, Insurance firms, etc, will have to adopt their

offerings to the new channel to take care of the uncertain future. Although the

immediate benefits of the technology may not look much due to various security

related and other issues, however, the potential that mobile access offers is

so great that FSPs will be forced to embrace it. Despite the initial reluctance

in adoption of the technology, the FSPs will have to follow a new multi-

platform strategy in offering their services. The reasons for the shift are not

hard to assess.

Instead of waiting for technologies to stabilize and giving mobile

delight to customers, it makes sense to deploy mobile applications now.

Mobile Access to Internet is increasing rapidly,

in general. Enterprises are already making plans to invest in mobile

technologies for mobile enabling their employees and customers for

business purposes. This will accelerate the demand for financial services on

mobile devices

The FSPs who start these services first will have the

advantage. Rather than waiting for conceptualizing a Killer Application,

it would be better to adapt to wireless within the constraints of the

technology. Besides the first mover advantage, this offers an experience with a

technology that is continuously happening and will be improving- if we go by the new evolving networks based on

increasingly powerful industry standards of GPRS, EDGE and UMTS. These are

leading to next generation of wireless networks called 3G, which can provide up

to 2 Mbps bandwidth. Hence, instead of waiting for technologies to stabilize

and then giving mobile delight to customers, it makes sense to deploy mobile

applications now.

Financial Services

Financial services can be segmented into Retail Banking, Retail

Broking, Investment Banking and Mobile

payments. Beside these FSP may be providing services related to Insurance,

Financial advising, Loans, Smart Cards, etc.

Survey data from TowerGroup says that users of

wireless financial services in World Regions will grow at a rapid pace,

reaching 35 million in North America and 77

million apiece in Western Europe and Asia

Pacific by 2005. The analyst reports indicate that any FSP cannot afford to

ignore the new channel. However, the question is what services to mobile enable

and how to mobile enable. Will there be sufficient ROI on the investment made

in the wireless applications? In the short term, it appears that profitable ROI

may not be there. However, it is important to invest now in this new

communication channel to the customers. An important reason is that, wireless

is not only going to take a share of the financial market its going to expand

the market as well. Customers, who are going to be more mobile in future,

cannot ignore the value of all-time banking services.

M-Commerce Value Chain

In any relationship between a customer and a business,

there are three levels. The first level is related to the content

provisioning about the business. This may be about the services offered by

the business or about the specific service that the customer is already

subscribing or buying from the business.

The second level is the transactional level, where

the customer has the option of initiating a business transaction with the

business or vice-versa. Growing to this level on a new channel of communication

requires a confidence about the security and authentication on both sides.

Also, both parties need to be confident about the stability of the channel.

The third level is the Relationship building when

both the customer and the business are confident of each other as well as

channel; both have experienced the transactional level to some extent.

In the financial services scenarios, customers getting

financial information on the hand held devices over wireless links, i.e., level

one is already a reality. Any FSP who has not reached this level is well

advised to start the wireless service.

Any FSP who has not reached Mobile

Content Provisioning level is well advised to immediately start the service.

One lesson of dot com burst was that one should exercise

caution while starting any technology based channel. Too much of caution in the

M-Commerce world may, however, lead to huge loss in revenues and also, what is

more dangerous, loss of customers to competitors who are more tech savvy in the

eyes of the customers.

The FSPs have to graduate to the second level quickly. The

second level is more difficult as it involves actual money changing hand in

each contact with the customer. It reduces the total cost of the transaction

for the FSP. However, it is more difficult to achieve because of security and

limitations of the devices. We understand that by end 2002 this level will be

attained by most of the financial institutions. However, the profitability may

require adoption by consumers in large numbers.

The ultimate goal of all FSPs, is to enable single

click transactions, live advice, location specific transactions, personal

mobile advertising and third party sales from the mobile device. This level

will require mobile applications and infrastructure that guarantees more

security, customization, location-based actions, time sensitivity,

device-neutrality and easy of action. The FSPs would be able to graduate to

this level within a year, i.e., by the start of 2003. Although the schedule

given here looks tight, we believe that the investments already made by the

Wireless Service Providers (WSP) in the infrastructure will require them to

search for services that can lead to customer ownership. In their search the

WSPs will have to hit on the financial services to get the ROIs. The FSP anyway

will strive to move up the value chain of the m-Commerce. This interplay of

WSPs and FSPs will create more value for money for customers, as they will get

the benefits and convenience of wireless banking on a continuous basis. Initial

revenues, however, will be reaped by the WSPs. As per a Gartner prediction last

year, WSPs will be the real beneficiaries of

the financial data services. For FSPs the wireless

delivery channel only adds to the total cost. FSPs are actually in a catch-22

situation. They have to invest in non-paying wireless services or else they

will be at a considerable competitive disadvantage. This situation will

continue till the end of this year. However, we believe that 2003 is the year

of wireless financial services.

Given the scenario described above what should be the

strategy of the FSPs in adapting to the wireless technology.

Success Strategy

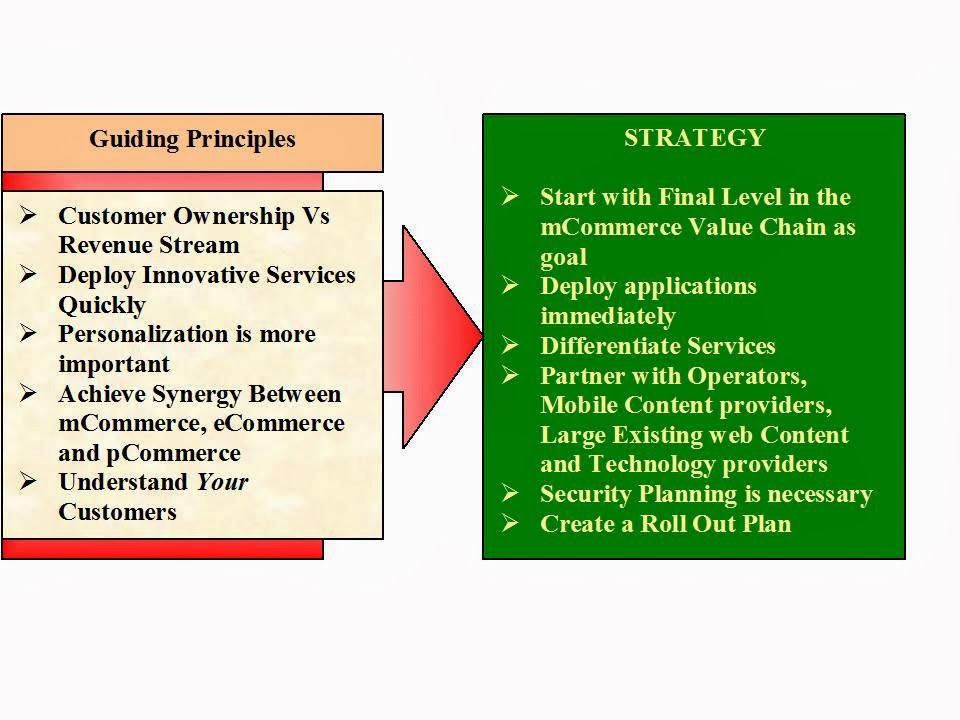

Before defining any grand strategy, it is imperative to

understand the guiding principles that should drive that strategy. The importance

that the FSPs should give to customer retention and ownership should be more

than that given to revenue stream. The applications need to be innovative and

should be quickly deployed. Any service provided to the customers on mobile

devices should be personalized as the mobile device is considered very personal

especially in Asian and Japanese geographies. FSPs should strive to achieve

synergy between physical, electronic and mobile commerce. This synergy should

create a holistic strategy for the FSP.

The basic point is that the strategy should be geared towards the

specific customer profiles of the FSP. It should be mentioned that unique

profile of the customers for the specific FSPs is a major factor affecting the

mobile strategy.

We propose at the broad level the strategy in embracing

mobile technologies for the FSPs. The FSP should start with a goal of achieving

the highest level in the mCommerce value chain. Rather than waiting for

markets, technologies and wireless services to improve, it is imperative that

applications should be deployed quickly. Taking care of competition, as far as

possible, differentiate the services. Continuous innovation in differentiation

is the crux of the matter.

The FSP should start with a goal of achieving the highest level in

the mCommerce value chain.

Most important point in the strategy is the collaboration

that should be achieved with all players across infrastructure value chain.

This includes tie-ups with Operators, Mobile Content providers, Existing Web

Content providers and technology providers.

However, the weakest link in the whole process, i.e.,

end-to-end security, should be properly planned. This planning may require

readiness to pay for security breaches.

Taking all of these things into account a Roll Out plan of

applications at each point of the value chain should be made and executed.

Conclusions

FSPs cannot afford to ignore the wireless channel to the

customers and employees. The channel will require services to be offered to the

customers. The levels of value defined for mCommerce starts with the

information provisioning and ends at the mobile Customer Relationship

Management (mCRM). By the end of this year, most of financial institutes would

have moved up to the second level of transaction-enabled services. We believe

that by 2003 the mCRM will provide the key competitive advantage to FSPs.

A Roll out plan of financial applications keeping the

above scenario in consideration is the major decision that FSPs need to take

NOW.